声明

本文代码均保存在

https://github.com/super-213/business_data_analysis

有需要的可以自行下载

查看数据

1

2

| df = pd.read_excel('客户信息及违约表现.xlsx')

df.head()

|

| 收入 |

年龄 |

性别 |

历史授信额度 |

历史违约次数 |

是否违约 |

| 462087 |

26 |

1 |

0 |

1 |

1 |

| 362324 |

32 |

0 |

13583 |

0 |

1 |

| 332011 |

52 |

1 |

0 |

1 |

1 |

| 252895 |

39 |

0 |

0 |

1 |

1 |

| 352355 |

50 |

1 |

0 |

0 |

1 |

缺失值处理

异常值处理

1

2

3

4

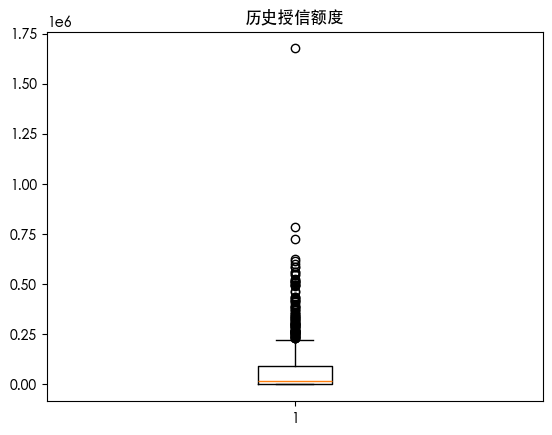

| for col in df.columns:

plt.boxplot(df[col])

plt.title(col)

plt.show()

|

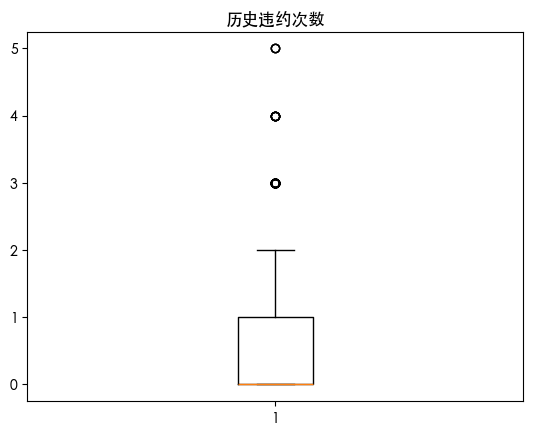

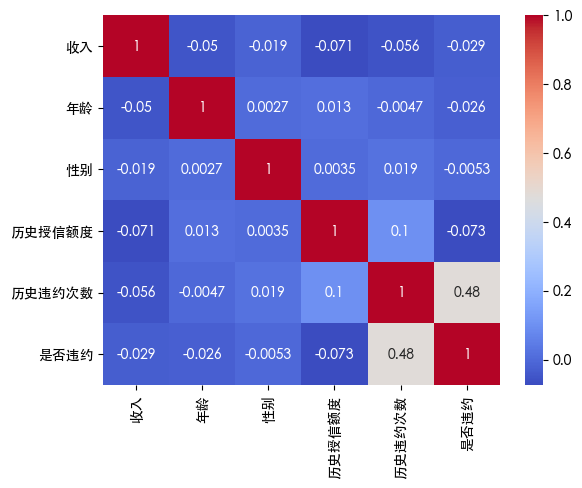

发现两个特征存在异常值 使用热力图查看特征之间的关系

1

2

3

4

| import seaborn as sns

sns.heatmap(df.corr(), annot=True, cmap='coolwarm')

plt.show()

|

看到 历史违约次数和是否违约相关性很大 并且历史违约次数存在异常值 因此新增此特征的异常值特征列

1

2

3

4

5

6

7

8

9

10

11

12

| col = '历史违约次数'

Q1 = df[col].quantile(0.25)

Q3 = df[col].quantile(0.75)

IQR = Q3 - Q1

lower_bound = Q1 - 1.5 * IQR

upper_bound = Q3 + 1.5 * IQR

df[f'{col}_is_outlier'] = ((df[col] < lower_bound) | (df[col] > upper_bound)).astype(int)

df = df.drop(columns=['历史授信额度'])

|

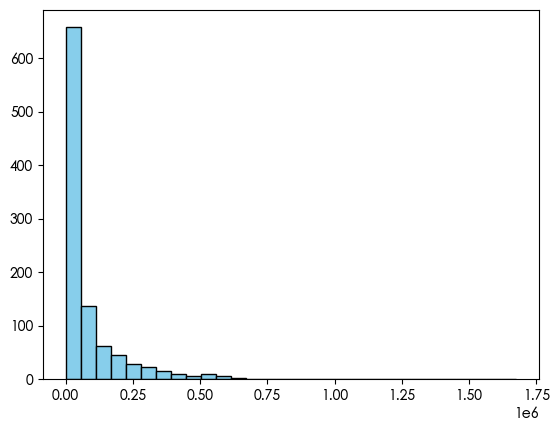

继续查看另一个异常值的特征分布

1

2

| plt.hist(df['历史授信额度'], bins=30, color='skyblue', edgecolor='black')

plt.show()

|

可以看到 数据是右偏的 并且是长尾分布 对于此数据 使用对数变换

1

2

3

| import numpy as np

col = '历史授信额度'

df[f'{col}_log'] = np.log1p(df[col])

|

数据划分

1

2

3

4

5

| X = df.drop(columns=['是否违约'])

y = df['是否违约']

from sklearn.model_selection import train_test_split

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.2, random_state=42)

|

XGBoost

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

| from xgboost import XGBClassifier

xgb = XGBClassifier(

n_estimators=100,

learning_rate=0.1,

max_depth=5,

subsample=0.8,

colsample_bytree=0.8,

random_state=42

)

xgb.fit(X_train, y_train)

y_pred = xgb.predict(X_test)

from sklearn.metrics import classification_report, confusion_matrix

print(confusion_matrix(y_test, y_pred))

print(classification_report(y_test, y_pred))

|

| 实际 \ 预测 |

0 |

1 |

| 0 |

110 |

9 |

| 1 |

29 |

52 |

| 类别 |

Precision |

Recall |

F1-Score |

Support |

| 0 |

0.79 |

0.92 |

0.85 |

119 |

| 1 |

0.85 |

0.64 |

0.73 |

81 |

| accuracy |

|

|

0.81 |

200 |

| macro avg |

0.82 |

0.78 |

0.79 |

200 |

| weighted avg |

0.82 |

0.81 |

0.80 |

200 |

LGBM

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

| from lightgbm import LGBMClassifier

lgbm = LGBMClassifier(

n_estimators=100,

learning_rate=0.1,

max_depth=5,

subsample=0.8,

colsample_bytree=0.8,

random_state=42

)

lgbm.fit(X_train, y_train)

y_pred = lgbm.predict(X_test)

from sklearn.metrics import classification_report, confusion_matrix

print(confusion_matrix(y_test, y_pred))

print(classification_report(y_test, y_pred))

|

| 实际 \ 预测 |

0 |

1 |

| 0 |

113 |

6 |

| 1 |

29 |

52 |

| 类别 |

Precision |

Recall |

F1-Score |

Support |

| 0 |

0.80 |

0.95 |

0.87 |

119 |

| 1 |

0.90 |

0.64 |

0.75 |

81 |

| accuracy |

|

|

0.82 |

200 |

| macro avg |

0.85 |

0.80 |

0.81 |

200 |

| weighted avg |

0.84 |

0.82 |

0.82 |

200 |

随机森林

1

2

3

4

5

6

7

8

9

10

11

12

13

| from sklearn.ensemble import RandomForestClassifier

rm = RandomForestClassifier(

n_estimators=100,

max_depth=5,

random_state=42

)

rm.fit(X_train, y_train)

y_pred = rm.predict(X_test)

from sklearn.metrics import classification_report, confusion_matrix

print(confusion_matrix(y_test, y_pred))

print(classification_report(y_test, y_pred))

|

| 实际 \ 预测 |

0 |

1 |

| 0 |

117 |

2 |

| 1 |

29 |

52 |

| 类别 |

Precision |

Recall |

F1-Score |

Support |

| 0 |

0.80 |

0.98 |

0.88 |

119 |

| 1 |

0.96 |

0.64 |

0.77 |

81 |

| accuracy |

|

|

0.84 |

200 |

| macro avg |

0.88 |

0.81 |

0.83 |

200 |

| weighted avg |

0.87 |

0.84 |

0.84 |

200 |

贝叶斯

1

2

3

4

5

6

7

8

9

| from sklearn.naive_bayes import GaussianNB

nb = GaussianNB()

nb.fit(X_train, y_train)

y_pred = nb.predict(X_test)

from sklearn.metrics import classification_report, confusion_matrix

print(confusion_matrix(y_test, y_pred))

print(classification_report(y_test, y_pred))

|

| 实际 \ 预测 |

0 |

1 |

| 0 |

111 |

8 |

| 1 |

43 |

38 |

| 类别 |

Precision |

Recall |

F1-Score |

Support |

| 0 |

0.72 |

0.93 |

0.81 |

119 |

| 1 |

0.83 |

0.47 |

0.60 |

81 |

| accuracy |

|

|

0.74 |

200 |

| macro avg |

0.77 |

0.70 |

0.71 |

200 |

| weighted avg |

0.76 |

0.74 |

0.73 |

200 |

逻辑回归

1

2

3

4

5

6

7

8

9

| from sklearn.linear_model import LogisticRegression

lr = LogisticRegression()

lr.fit(X_train, y_train)

y_pred = lr.predict(X_test)

from sklearn.metrics import classification_report, confusion_matrix

print(confusion_matrix(y_test, y_pred))

print(classification_report(y_test, y_pred))

|

| 实际 \ 预测 |

0 |

1 |

| 0 |

88 |

31 |

| 1 |

60 |

21 |

| 类别 |

Precision |

Recall |

F1-Score |

Support |

| 0 |

0.59 |

0.74 |

0.66 |

119 |

| 1 |

0.40 |

0.26 |

0.32 |

81 |

| accuracy |

|

|

0.55 |

200 |

| macro avg |

0.50 |

0.50 |

0.49 |

200 |

| weighted avg |

0.52 |

0.55 |

0.52 |

200 |

模型横向对比

XGBoost

- 整体表现: Accuracy = 0.81

- 优点:

- Precision 对 1 类 较高 (0.85),但 Recall 偏低 (0.64)

- 说明它比较谨慎 预测为违约时大多是真的(低假阳性)但漏掉了不少实际违约(高假阴性)

- 适合在误判正常人为违约成本高的场景

LightGBM

- 整体表现: Accuracy = 0.82(略高于 XGB)

- 优点:

- 对类别 1 的 Precision 更高 (0.90) Recall 同样偏低 (0.64)

- 预测结果更保守 对 1 的识别严格 但仍漏掉一部分违约客户

- 对比 XGBoost:性能非常接近,但 LightGBM 对类别 0 的 Recall 更高 对正常客户的识别更稳

随机森林

- 整体表现: Accuracy = 0.84

- 优点:

- 类别 0 的 Recall 极高 几乎不会把正常客户错判为违约

- 类别 1 的 Precision 很高 (0.96),但 Recall 仍然只有 0.64 但还是漏掉部分

- 特点:

- Bagging 思路让它在这类低维表格数据上表现最稳健。

- 如果更在意总体准确率和稳健性,随机森林是首选。

朴素贝叶斯

- 整体表现: Accuracy = 0.74

- 优点: 对类别 0 Recall 较高

- 缺点: 类别 1 Recall 低 几乎一半违约客户都漏掉。

- 原因:

- 假设特征独立,这在客户数据里往往不成立 会导致性能下降

逻辑回归

- 整体表现: Accuracy = 0.55

- 缺点:

- 类别 1 的 Recall 极低 大部分违约客户被判成了正常

- 说明数据中的关系并不是线性可分的 逻辑回归模型过于简单

- 适用场景:

- 在数据高度线性且变量少时可用 但在这个复杂数据集上严重欠拟合

总结

| 模型 |

Accuracy |

类别 1 (违约) Recall |

特点 |

| 随机森林 |

0.84 |

0.64 |

最优表现,稳健,几乎不误判正常客户 |

| LightGBM |

0.82 |

0.64 |

高效,Precision 高,Recall 偏低 |

| XGBoost |

0.81 |

0.64 |

与 LGBM 接近,偏保守 |

| 朴素贝叶斯 |

0.74 |

0.47 |

偏弱,假设不符合实际 |

| 逻辑回归 |

0.55 |

0.26 |

严重欠拟合,不适合此任务 |

结论:

- 整体上 树模型(RF、XGB、LGBM)表现远优于线性模型(LR)和简单概率模型(NB)

- 随机森林在这里是最佳选择,因为它在准确率和稳定性上均优 并且对违约的准确率特别高

- 但三种树模型都有一个共性:违约 Recall 偏低(都在 0.64 左右) 意味着有不少违约客户没被识别出来